Retirement: "Establish Lifetime Annuity and Account Based Pension"

ℹ️ Strategy Information

Strategy Name: Establish Lifetime Annuity (30%) and Account Based Pension (70%)

Type of Strategy: Retirement

Impact on modelling: When selected, this strategy splits the member’s superannuation balance between a Lifetime Annuity and an Account Based Pension. The Lifetime Annuity provides an income payment until life expectancy and the Account Based Pension provides a second income payment with both income payments appearing in the Cashflow table.

📺 Watch our Annuity Case Study

View our case study here on a comparison of Annuities and Account Based Pensions.

ℹ️ How to add the Annuity to your Strategy List

Admin users will be able to navigate to Settings > Strategy List and drag the strategy titled Establish Lifetime Annuity (30%) and Account Based Pension (70%) across to the right (i.e. the Selected pane) then hit save. The Annuity strategy will then be available in newly created Strategy Builder scenarios.

ℹ️ How to use the strategy:

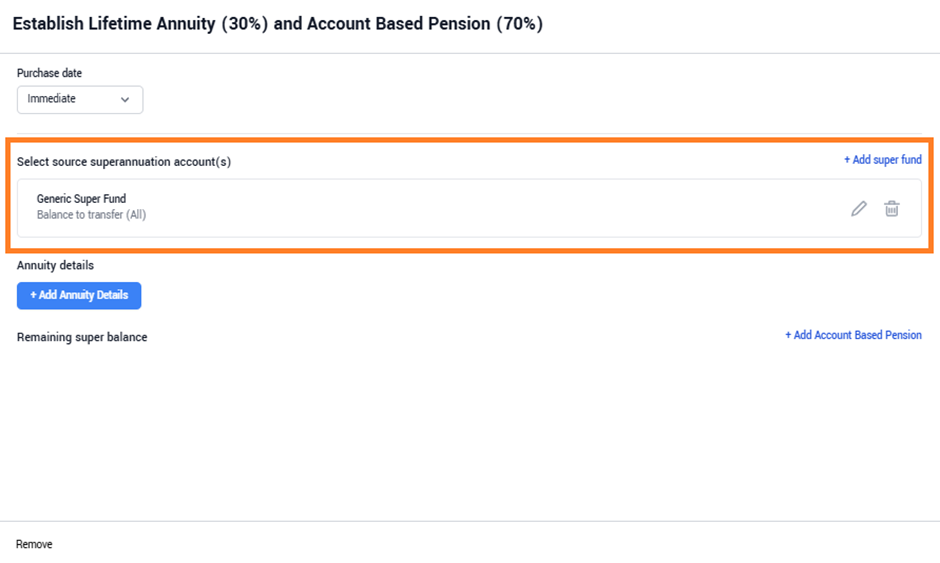

- Within your scenario, add and edit the Annuity strategy. The default super fund from the fact find will automatically appear as the source Super Account. The user can add other Super Accounts if additional accounts need to be transferred.

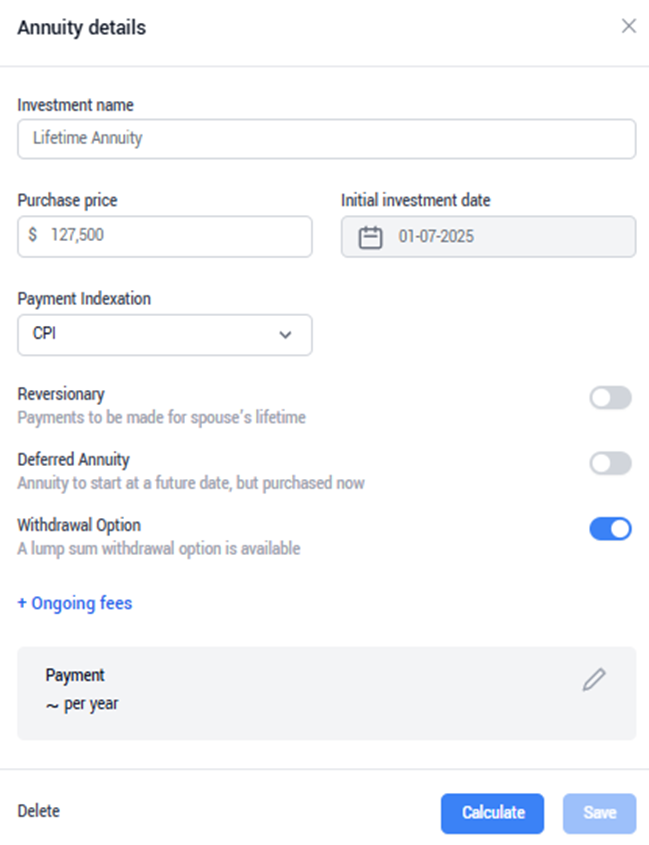

- Click +Add Annuity Details to add the Annuity and enter a name for the investment. By default the strategy will calculate 30% of the Super balance and update the Purchase price (can be overridden if required).

- Select the Payment Indexation options from the following:

• Nil - No indexation is applied to the calculated payment rate

• CPI - The inflation rate specified within Settings > Portfolios is applied to the calculated payment rate each month.

• Market-Linked - Payment rate is indexed in line with the expected returns of the selected investment option.

• Other - User can specify % rate to be applied to the payment each month. Please note that selection of this option will not provide a calculated payment rate.

- Select other annuity options as follows:

• Reversionary – When selected payments end at spouse's lifetime. Note the payment rate may differ with this option toggled on/off.

• Deferred Annuity – Toggle this option on to defer the income of the Annuity, a payment rate would need to be manually entered when this is selected. Refer to your product provider for the correct payment to apply.

• Withdrawal Option - When selected, a capital amount equal to the purchase price will be displayed in the Annuity Withdrawal Value chart and shown as the withdrawal value. This amount will gradually decrease to $0 by the member's life expectancy. Additionally, a Death Value will be activated, remaining equal to the purchase price until the member reaches half of their life expectancy. After that point, the Death Value will decline in line with the withdrawal value.

• Ongoing Fees - Adding an ongoing fee will deduct the amount from the annuity income payment before the payment enters the household bank account.

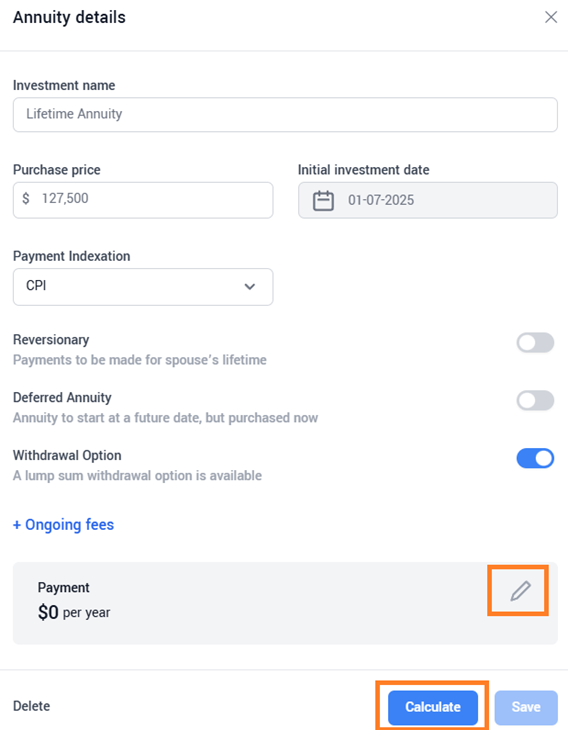

- Once the above options have been adjusted, users can hit Calculate. This will use the Challenger Payment Rate Tables to provide a payment amount per year. Note this is currently only connected to a partial table so in some instances users may receive a $0 value after selecting Calculate. In this instance users will need to refer to the product provider and manually enter in the correct payment amount by using the edit function (pencil icon). Once the correct payment rate has been calculated or input, ensure you hit Save.

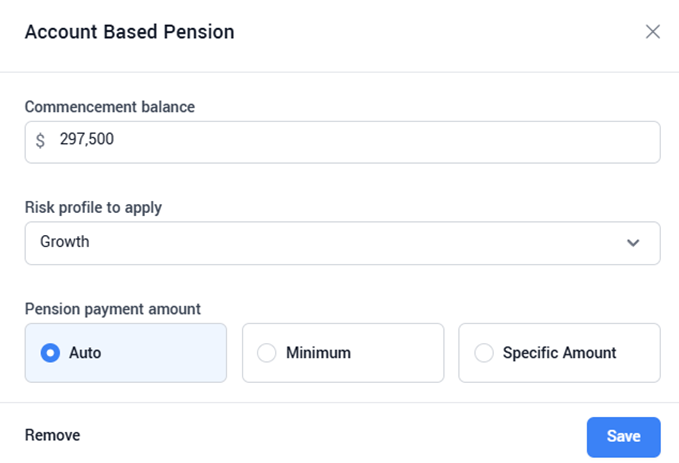

- Allocate the remaining super balance to the Account Based Pension by selecting + Add Account Based Pension and complete the following.

- Select the Risk Profile to apply: Users will have the choice to select the risk profile for the Account Based Pension, because only a portion of the Super Funds are transferred into the Account Based Pension, generally a higher exposure is recommended to ensure the clients overall investments align with their risk profile.

- Select the Pension payment amount:

• Auto - System will calculate the amount to drawdown (if above the minimum) in order to meet expenses

• Minimum - System will drawdown the minimum rate required based on their age.

• Specific Amount - User can specify an amount to drawdown.

- Once the above Account Based Pension has been added, hit Calculate then Save & Next to update the strategy text.

📈Demonstrating the benefits of an Annuity

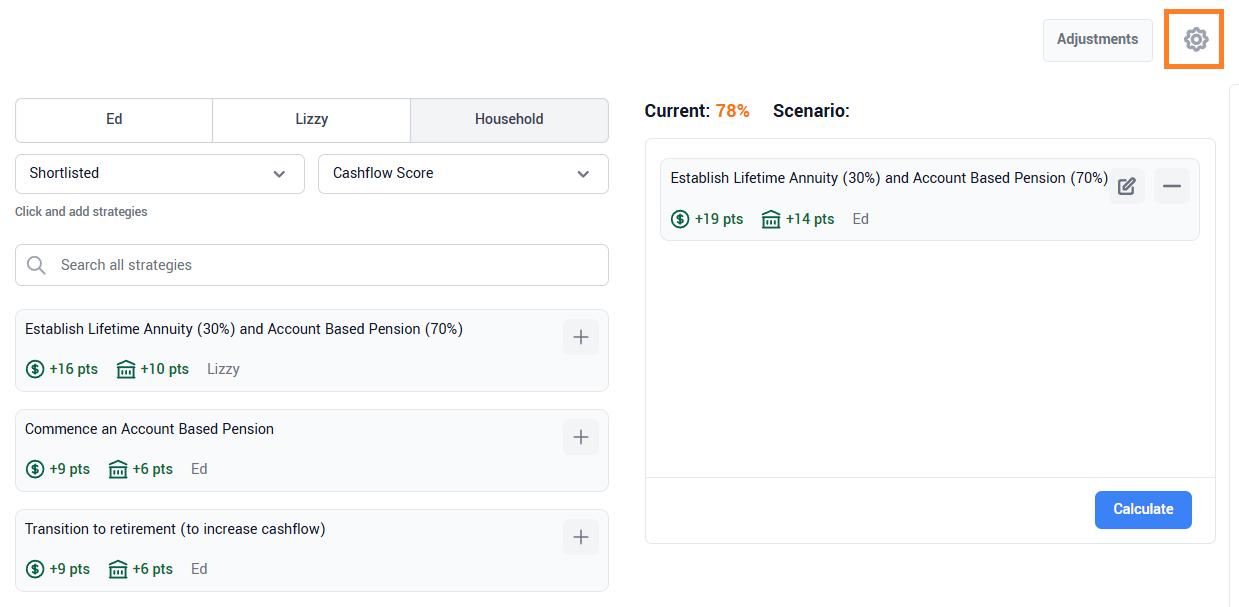

To clearly show the longevity benefits of an annuity, users can manually update the life expectancy of the client to extend out the projection period in the event the client outlives their life expectancy. To do this, use the settings option (cog icon) within your scenario (see screenshot below).

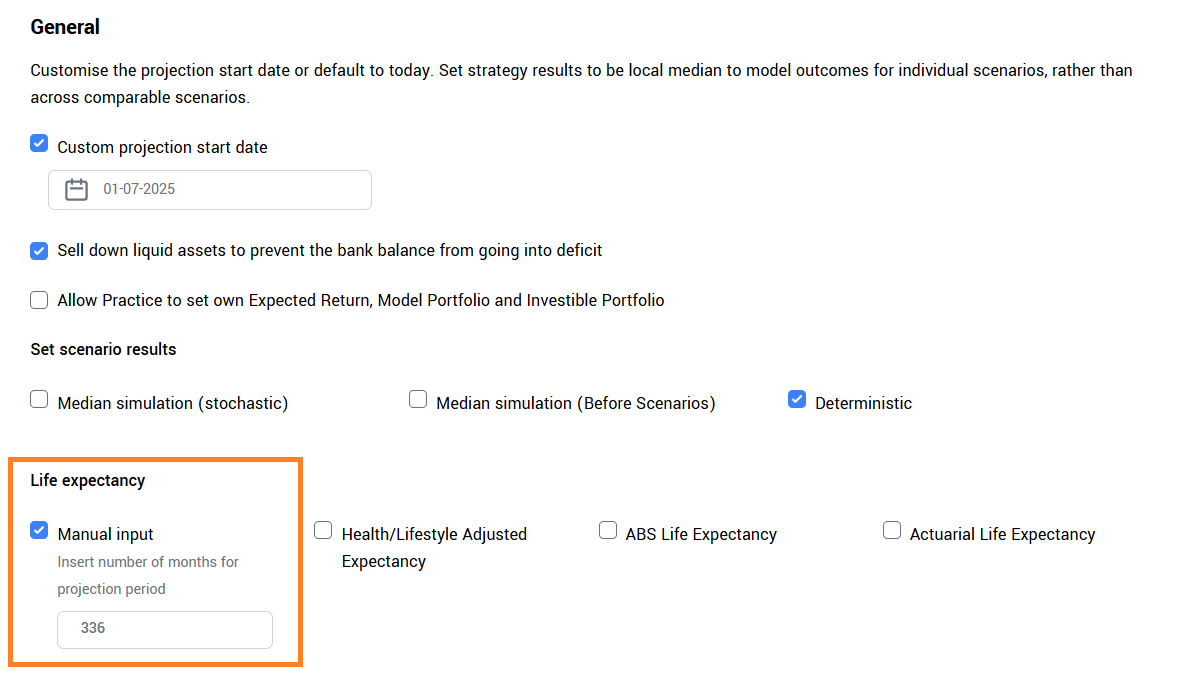

Scroll down to the General section and under Life expectancy select Manual Input. The user can then input the number of months for the total projection period. Ensure you scroll down to the end of the page and hit save.

❗Ensure these changes are made to all scenarios to ensure your comparisons are consistent (i.e. Update Before scenario settings and any recommended/proposed).

Users can then visualise the benefits of an annuity by selecting View Modelling against any scenario and using the available charts/tables.

View our Annuity case study here